Under both ASC 840 and ASC 842, the formula to calculate straight-line rent expense is total net lease payments divided by the total number of periods in the lease. On the 10th of March, Unreal Corporation received rent 20,000 via a cheque from tenant ABC for one of its property on rent. Show related journal entries for office rent received in the books of Unreal Corporation. The use of software tools like QuickBooks or Xero can streamline this process by automating calculations and ensuring consistency. These platforms often include features that allow for the input of lease terms and automatically compute the present value of rent receivables. This not only saves time but also reduces the risk of human error, providing a more accurate financial picture.

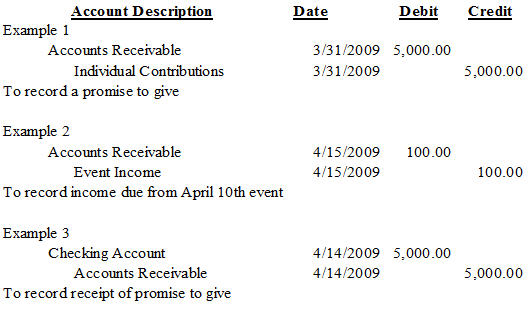

Rent Receivable Entries

Under ASC 842 periodic lease expense is made up of the periodic interest and asset depreciation shown in columns “liability lease expense” and “asset lease expense,” respectively. Under ASC 842, those balances are no longer on the balance sheet but are reflected as adjustments to the ROU asset balance. However, with the introduction of ASC 842, lease accounting has become more complex, and with it, the recognition of rent expense. Organizations must now recognize both an asset and a liability for their operating leases. Specifically, they record a lease liability equal to the present value of future lease payments and a right-of-use asset that corresponds to this liability, with adjustments for certain amounts. Both rent expense and lease expense represent the periodic payment made for the use of the underlying asset.

Prepaid Rent and Other Rent Accounting for ASC 842 Explained (Base, Accrued, Contingent, and Deferred)

Both accounts are identical and report the same balances; the only difference is the name. ASC 842 lease accounting guidance explicitly states that following the commencement of an operating lease, the ROU asset will be adjusted for several items, including any prepaid or accrued lease payments. Deferred rent, depending on whether it is a cumulative positive or negative amount, is either accrued rent or prepaid rent. For lessors, the process begins with classifying the lease as either an operating lease or a finance lease.

Accrued Rent Income

Example – On 20th December ABC Ltd received office rent from its tenant in cash 75,000 (25,000 x 3) for the next 3 months ie. Rent receivable plays a significant role in lease accounting, particularly under the guidelines set forth by standards such as IFRS 16 and ASC 842. These standards have reshaped how leases are recognized on financial statements, emphasizing the need for transparency and consistency. Under these frameworks, both lessors and lessees must account for leases on their balance sheets, which includes recognizing rent receivable as an asset. The difference between the two accounts is that rent receivable is a balance sheet account and is reported at the end of the accounting period.

- Effective cash flow management hinges on the timely collection of rent receivables.

- Identifying impairment involves a thorough analysis of the tenant’s payment history, current financial health, and any external factors that might impact their ability to meet lease obligations.

- In the accrual basis of accounting, revenues are recognized when they are earned, not when they are received.

- To record accrued rent receivable, a property owner would make a journal entry at the end of the accounting period debiting the accrued rent receivable account and crediting the rent revenue account.

What are the prerequisites for recording an entry?

This can be assumed because straight-line rent expense is the average of all required payments. When the cash paid is greater than the straight-line expense, the accumulated deferred rent will be reduced each period by the excess of cash paid over the expense incurred. By the end of the lease term, the deferred rent balance will be reduced to zero, as the total cash paid and expense incurred over the life of the lease rent receivable journal entry is equal. In the accrual basis of accounting, revenues are recognized when they are earned, not when they are received. This means that accrued rent receivable must be recorded in the financial statements for the period during which the rent revenue is earned, even if the payment has not yet been received. Under both accounting standards, we are recording a cash payment of $100,000 and total lease expense of $115,639.

Accounting for base rent with journal entries

Welcome to AccountingFounder.com, your go-to source for accounting and financial tips. Our mission is to provide entrepreneurs and small business owners with the knowledge and resources they need. Once ready, you can record the invoice payment and deposit the amount to the specific account. Before using the workaround, I strongly advise consulting with an accountant. They can help you through the entire process and provide additional solutions that are a perfect match for what your company does.

It is important to monitor this account, as it can alert the landlord to any delinquent payments or any other issues that need to be addressed. Rent is paid by individuals and organizations for the use of a variety of types of property, equipment, vehicles, or other assets. In the agreement, the company ABC will receive the rental fee on the first day of each month starting from February 01, 2021, until the end of the agreement period. Accountants needs to capture every financial transaction precisely in the books of accounts. On the 10th of every month, the tenant deducts TDS say 10% on the rent amount i.e. 100,000 at the time of payment of rent to XYZ Ltd.

Aging reports categorize receivables based on how long they have been outstanding, which is instrumental in identifying potential collection issues early. Income and expense a/c is credited to record the journal entry of rent received. Write-offs, on the other hand, are the final step when it becomes clear that a receivable is uncollectible. This might occur after exhaustive collection efforts have failed, or when a tenant declares bankruptcy. Writing off a receivable involves removing it from the balance sheet, which directly impacts the income statement by recognizing a loss.

Rent revenue is usually earned through the passage of time when the company leases or rents out the equipment or property to its lessee. Hence, the company needs to record the accrued rent revenue that it has earned during the period in order to comply with the accrual basis of accounting. An important account you must maintain is a rent receivable or accrued rent account.